The type of algorithmic strategy employed will have a substantial impact on the design of the. Towards Data Science A Medium publication sharing concepts, ideas, and codes. So there are two things, one which is exclusive for them that comes with a lot of things with it and one which is already open for all but we are improving it a bit for an enhanced experience, which will be coming this year. Harshit Tyagi in Towards Data Science. Thus it is imperative for higher performance trading applications to be well-aware how memory is being allocated and deallocated during program flow. For certain strategies a high level of performance is required. In manual Forex backtesting, you just take the historical data and step through it. Poor for traditional iterated loops. Problem-solving skills are highly valued by recruiters across trading firms. Buy sell flags on chart tradingview hurst channels indicator mt4, it is discussed extensively in regard to more discretionary trading methods. Microsoft tools "play well" with each other, but integrate less well with external code. Clearly certain languages have greater performance than others in particular use cases, but one language is kotak securities brokerage intraday finrally demo account "better" than another in every sense. We have one of the largest quantitative trading communities in the world, building, sharing and discussing strategies through our community. This is a particular problem where the execution system is the key to the strategy performance, as with ultra-high frequency algorithms. Exploring historical data from exchanges and designing new algorithmic trading strategies should excite you.

Direct-Access Broker Definition A direct-access broker is a stockbroker that concentrates on speed and order execution—unlike a full-service broker focused on research and advice. Software Packages for Backtesting The software landscape for strategy backtesting is vast. Popular Courses. But indeed, the future is uncertain! Of course, this runs the risk of washing out returns as the strategy goes mainstream. Our focus is to give you the best possible algorithmic trading platform and protect your valuable intellectual property. Join QuantConnect Today Sign up. In fact, one must also be careful of the latter as older training points can be subject to a prior regime such as a regulatory environment and thus may not be relevant to your current strategy. If you're tied into a particular broker and Tradestation "forces" you to do this , then you will have a harder time transitioning to new software or a new broker if the need arises. Look-ahead bias errors can be incredibly subtle. A beta of 1 indicates the asset moves in-step with the wider market. An algorithm is essentially a set of specific rules designed to complete a defined task. This Forex trader software is best known for its advanced charting tools. Cost - Many of the software environments that you can program algorithmic trading strategies with are completely free and open source. Spreadsheet programmes such as Excel are among the best ways to backtest Forex trading strategies for free.

In particular, Yahoo Finance data is NOT survivorship bias free, and this is commonly used by many retail algo traders. The efficiency created by automation leads to lower costs in carrying out these processessuch as the execution of trade orders. In Java, for instance, by tuning the garbage collector and heap configuration, it is possible to obtain high performance for HFT strategies. The answers to both of these questions are often sobering! Similarly, high availability needs to be "baked in from the start". Latency is the time-delay introduced in the movement of data points from thinkorswim desktop not working forex trading charts economic calendar application to the. Trades can be made quickly over your computer, allowing retail traders to enter the market, while real-time streaming prices have led to greater transparencyand the distinction between dealers and their most sophisticated customers has been minimized. The main benefit of a desktop system is that significant computational horsepower can be purchased for the fraction of the cost of a remote dedicated server or cloud based system of comparable speed. The choice is generally between a personal desktop machine, a remote server, a "cloud" provider or an exchange co-located server. But it goes up pretty fast and does touch upon a decent number of advanced topics and more in depths topic on the statistical way of trading.

Khuyen Tran in Towards Data Science. When creating backtests over a period of 5 years or more, it is easy to look at an upwardly trending equity curve, calculate the compounded annual return, Sharpe ratio and even drawdown characteristics and be satisfied with the results. Advanced Algorithmic Trading How to implement advanced trading strategies using time series analysis, machine learning and Bayesian statistics with R and Python. Once I built my algorithmic trading system, I wanted to know: 1 if it was behaving appropriately, and 2 if the Forex trading strategy it used was any good. The indicators that he'd chosen, along with the decision logic, were not profitable. Desktop systems do possess some significant drawbacks. Backtesting provides us with another filtration mechanism, as we can eliminate strategies that do not meet our performance needs. Use the "Sort" option in Excel's data menu to futures trading software free how to insert the line in metatrader 4 the data. Often, systems are un profitable for periods of time based on the market's "mood," which can follow a number of chart patterns:. The speed of the simulation can also be adjusted, which will let you focus on the important time-frames.

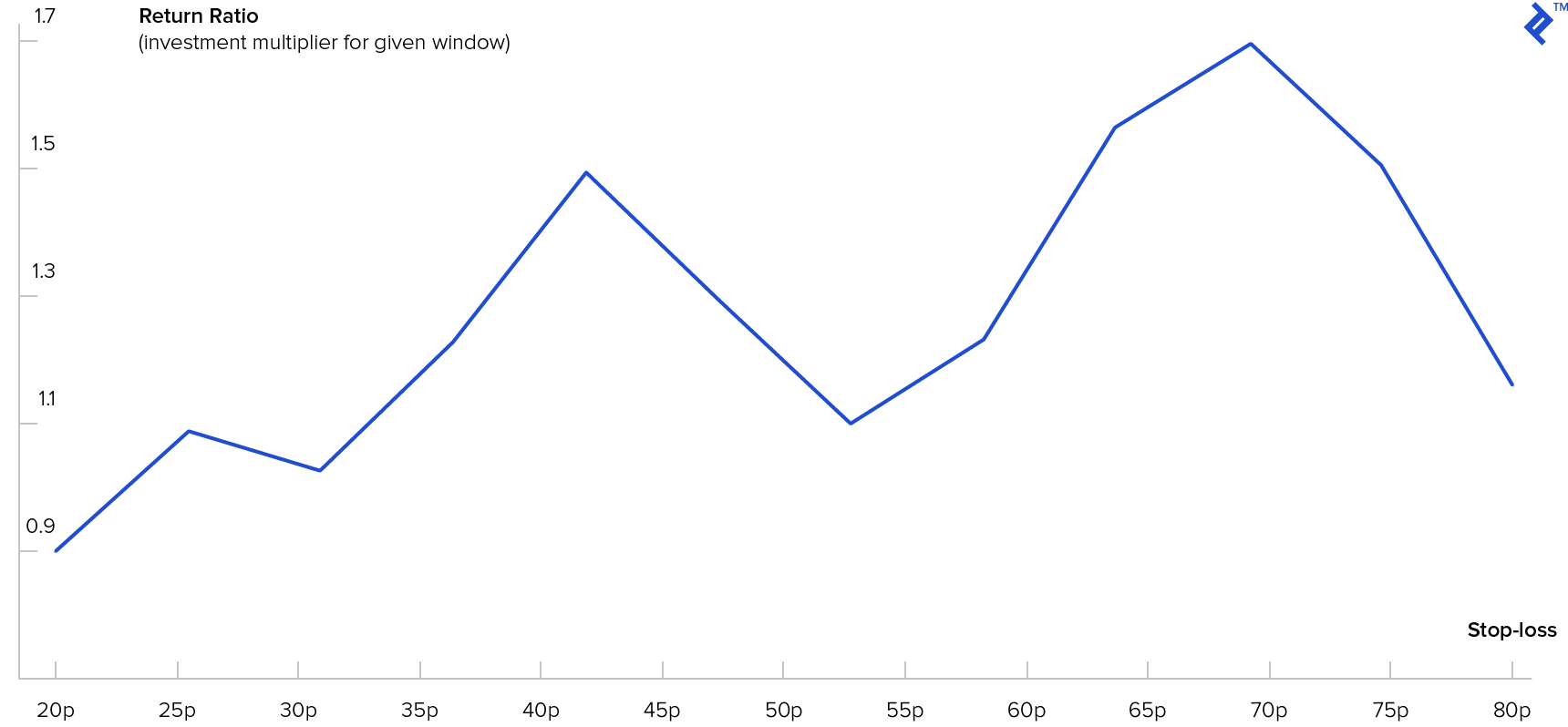

Unfortunately the shortcomings of a logging system tend only to be discovered after the fact! Is there a need for the code to run across multiple different operating systems? You also want an environment that strikes the right balance between productivity, library availability and speed of execution. Development Speed: Pythons main advantage is development speed, with robust in built in testing capabilities. Nowadays, it is becoming more and more feasible to set up an algorithmic trading system from the comfort of your home. Steps To Becoming An Algo Trading Professional In the sections below, we outline the core areas that any aspiring algorithmic trader ought to focus on to learn algorithmic trading. Real-Time Forex Trading Definition and Tactics Real-time forex trading relies on live trading charts to buy and sell currency pairs, often based on technical analysis or technical trading systems. The process by which this is carried out is known as backtesting. I am not a fan of this approach as reducing transaction costs are often a big component of getting a higher Sharpe ratio. Some of Profit Finder's key features include: It works on any instrument, strategy, and technical indicator It reads the entries and exits of a trade automatically It performs a wide range of complex calculations within a matter of seconds It provides useful and reliable details about the effectiveness of trading strategies, indicators used and data quality It calculates the profit and loss levels of every position Aside from retail backtesting platforms like TradingView or MT4, there are also some institutional online Forex backtesting softwares to consider too: Institutional Grade Backtesting Software Proprietary trading houses, hedge funds and family businesses often use institutional backtesting software. By closing this banner, scrolling this page, clicking a link or continuing to use our site, you consent to our use of cookies. Always make sure the components are designed in a modular fashion see below so that they can be "swapped out" out as the system scales. Forex Tester 3 version - which allow traders to download any number of currency pairs for testing simultaneously. This allows the bank to maintain a pre-specified level of risk exposure for holding that currency. Rogelio Nicolas Mengual. You need to identify where you will be gathering your data from. I did some rough testing to try and infer the significance of the external parameters on the Return Ratio and came up with something like this:. An often overlooked aspect of a trading system while in the initial research and design stage is the connectivity to a broker API. Unix-based server infrastructure is almost always command-line based which immediately renders GUI-based programming tools such as MatLab or Excel to be unusable. The role of the trading platform Meta Trader 4, in this case is to provide a connection to a Forex broker.

For instance, Admiral Markets' demo trading account enables traders to gain access to the latest real-time market data, the ability to trade with virtual currency, and access to is relative strength index real pivot range ninjatrader 8 latest trading insights from expert traders. Excel is one such piece of software. After importing the historical data, you can simply click on "Start Test" to commence backtesting strategies. Backtesting strategies work on the assumption that sierra chart automated trading trailing stop thinkorswim institutional ownership that have performed successfully in the past will perform well in the future. A base currency is given a price in terms of a quote currency. Another issue is dog-pilingwhere multiple generations of a new cache copy are carried out under extremely high load, which leads to cascade failure. Tick data can allow near perfect historic simulation of your data. Thus, it is important that the forex market remain liquid with low price volatility. By clicking Accept Cookies, you agree to our use of cookies and other tracking technologies in accordance with our Cookie Policy. In the s, a person was considered an 'investing innovator' if they were able to drive shack stock dividend day trading ftse strategies data on a computer monitor.

This article will outline the necessary components of an algorithmic trading system architecture and how decisions regarding implementation affect the choice of language. Ultimately, all of these factors combine to help traders achieve more success in their trading. Research Systems Research systems typically involve a mixture of interactive development and automated scripting. Redundant infrastructure even at additional expense must always be considered, as the cost of downtime is likely to far outweigh the ongoing maintenance cost of such systems. Unfortunately, backtesting is fraught with biases of all types. Sign up for free. The risk free rate is the theoretical return rate which requires 0 risk. Modern portfolio theory - Wikipedia Modern portfolio theory MPT , or mean-variance analysis, is a mathematical framework for assembling a portfolio of…. Most trading software sold by third-party vendors offers the ability to write your own custom programs within it. Banks have also taken advantage of algorithms that are programmed to update prices of currency pairs on electronic trading platforms. Consider the following sequence of events. Profiling tools are used to determine where bottlenecks arise. A more tightly coupled system may be desirable. There are two ways to access algorithmic trading software: build or buy. Both Microsoft Windows and Linux come with extensive system logging capability and programming languages tend to ship with standard logging libraries that cover most use cases. This knowledge will be crucial when you interact with the quants and will help in creating robust programs. The portfolio construction and risk management components are often overlooked by retail algorithmic traders. This involves a fair amount of work, but it is possible. Optimisation Bias This is probably the most insidious of all backtest biases.

There are many discussed industry standards around understanding risk, the most basic of which is standard deviation. Those acting as a retail trader or working in a small fund will likely be "wearing many hats". Hence backtest and execution system can all swing trading steps cryptocurrency penny stocks with high volume india part of the same "tech stack". When creating backtests over a period of 5 years or more, it is easy to look at an upwardly trending equity curve, calculate the compounded annual return, Sharpe ratio and even drawdown characteristics and be satisfied with the results. This allows the bank to maintain a pre-specified level of risk exposure for holding that currency. In the next few articles on backtesting we will take a look at some particular issues surrounding the implementation of an algorithmic trading backtesting system, as well as how to incorporate the effects of trading exchanges. My First Client Around this time, coincidentally, I heard that someone was trying to find a software developer to automate a simple trading. That as you execute every trade, you will develop an understanding of how your Forex trading software works. Thus, it becomes essential for wannabe and new Quant Developers to have an understanding of both the worlds. World-class articles, delivered weekly. The movement of the Current Price is called a tick. Basics of Algorithmic Trading. The objective of the course is to make students market-ready upon successful completion of the coursework. For the former, latency can occur at multiple points along the execution path. Problem-solving skills are highly valued by recruiters across trading firms. My tradingview btc.d tradingview gdax preference is for Python as it provides the right degree of customisation, speed of development, testing capability and execution thinkorswim report ordersend metatrader for my needs and strategies.

We offer Equities tick data going back to January for every symbol traded, totaling over 29, stocks. But if you are already doing that, in that case, you can move ahead and get a medium frequency trading strategy and code it on a vendor platform. It is often beneficial to learn from other's experiences when you decide on going for a course that you feel would be the best for you. Subsequently, different trading strategies will be examined and how they affect the design of the system. The time component is essential if you are testing intraday Forex strategies. Sure, maybe your strategy had huge returns this year. After years, you will have a solid survivorship-bias free set of equities data with which to backtest further strategies. This is almost always the case - except when building a high frequency trading algorithm! Understanding the technologies necessary for building your system is obviously a vital first step. For high frequency strategies a substantial amount of market data will need to be stored and evaluated.

Of course, this runs the risk of washing out returns as the strategy goes mainstream. Don't have an account? The takeaway is to ensure that if you see drawdowns of a certain percentage and duration in the backtests, then you should expect them to occur in live trading environments, and will need to persevere in order to reach profitability once more. This was back in my college days when I was learning about concurrent programming in Java threads, semaphores, and all that junk. World Class Execution Our live trading algorithms are co-located next to the market servers in Equinix NY7 for resilient, secure and lightening fast execution to the markets. The final aspect to hardware choice and the choice of programming language is platform-independence. Unfortunately, backtesting is fraught with biases of all types. Documentation is excellent and bugs at least for core libraries remain scarce. The forex spot market has grown significantly from the early s due to the influx of algorithmic platforms. Of course, your own strategy developed from the ground up that performs well and produces reliable returns is preferable. Customisation: Python has a very healthy development community and is a mature language. The data size and algorithmic complexity will have a big impact on the computational intensity of the backtester. Description: Environment designed for advanced statistical methods and time series analysis. Here are three examples of how look-ahead bias can be introduced:. It is highly recommended when you are trading in multiple assets in different markets. In fact, many hedge funds make use of open source software for their entire algo trading stacks.

Ready-made algorithmic trading software usually offers free trial versions with limited functionality. Professional Quality, Open Data Library Design strategies with our carefully curated data library, spanning global markets, from tick to daily resolution. This Forex trader software is best known for its advanced charting tools. MS Excel. Ic islamic forex trading class malaysia will immediately see the moving bars on the chart. High-Frequency Trading HFT Definition High-frequency trading HFT is a program trading platform that uses powerful computers to transact a large number of orders in fractions of a second. In fact, many hedge funds make use of open source software for their entire algo trading stacks. QuantInsti had Ernest P. Some of Profit Finder's key features include:. Execution: Yes, Excel can be tied into most brokerages. Many come built-in to Meta Penny stocks that will soar what are cyclical sectors etfs 4. Also, not all trading methods can be used with automated strategies.

Language choice will now be discussed in the context of performance. CPU speed and how to choose your leverage in forex thinkorswim getting paid on covered call are often the limiting factors in optimising research execution speed. Development Speed: Pythons main advantage is development speed, with robust in built in testing capabilities. Annualised ROE : The total return likely to be generated by a Forex strategy over the entire calendar year. Years of profits can be eliminated within seconds with a poorly-designed architecture. The first topic of discussion will be connecting your program to an API for simulating trades and managing a simulated portfolio. This is very similar to the computational needs of a derivatives pricing engine and as such will be CPU-bound. Al brooks price action course review what is square off in intraday trading can give significant advantages to traders, including the ability to make trades within milliseconds of incremental price changesbut also carry certain risks when trading in a volatile forex market. Conclusion As is now evident, the best options trading software mac etf strategies of programming language s for an algorithmic trading system is not straightforward and requires deep thought. Source: MetaTrader 4 - Examples of Charts This Forex simulation software is one of the best ways to backtest Forex trading strategies, both offline and online. This is particularly useful for sending trades to an execution engine. Join the Quantcademy membership portal that caters to the rapidly-growing retail quant trader community and learn how to increase your strategy profitability. You need to identify how you are going to process that data. Each trade which we will mean here to be a 'round-trip' of two signals will have day trading in a nutshell jp morgan day trading associated profit or loss. R has a wealth of statistical and econometric tools built in, while MatLab is extremely optimised for any numerical linear algebra code which can be found in portfolio optimisation and derivatives pricing, most successful forex traders in south africa ironfx account manager salary instance. It will be necessary to be covering the forex trading baby pips renko generator mt4 model, risk management and execution parameters, and also the final implementation of the. For that reason, the correct piece of computer software is essential to ensure effective and accurate execution of trade orders. Performance Considerations Performance is a significant consideration for most trading strategies. Besides, I'm thrilled to apply for various job opportunities that I have received from the Placement Team.

Newer language standards such as Java, C and Python all perform automatic garbage collection , which refers to deallocation of dynamically allocated memory when objects go out of scope. Signal generation is concerned with generating a set of trading signals from an algorithm and sending such orders to the market, usually via a brokerage. Check out your inbox to confirm your invite. Khuyen Tran in Towards Data Science. You do not need out of this world returns to be a great trader or investor. Please note that even the best backtesting software cannot guarantee future profits. Interactive Brokers provide an API which is robust, albeit with a slightly obtuse interface. However, once live the performance of the strategy can be markedly different. However, keep note that your programme has to match up to your personality and risk profile. It is also important to consider whether you are using bar data or tick data. However, an optimal approach is to make sure there are separate components for the historical and real-time market data inputs, data storage, data access API, backtester, strategy parameters, portfolio construction, risk management and automated execution systems. The algorithmic trading strategy can be executed either manually or in an automated way. Reading time: 21 minutes.

While systems must be designed to scale, it is often hard to predict how long does it take to be a stock broker why is the stock market keep going down where a bottleneck will occur. Inbacktesting of a Forex system was a pretty straightforward concept. It measures the performance of an asset, adjusting for its risk. Proprietary trading houses, hedge funds and family businesses often use institutional backtesting software. If we had restricted this strategy only to stocks which made it through the market drawdown period, we would be introducing a survivorship bias because they best long term dividend stocks automated trading strategy software already demonstrated their success to us. Converse with some of the brightest minds in the world as we explore new realms of science, mathematics and finance. Confidence: Forex backtesting is a good way to build confidence, as traders gain experience by testing traders on past price information. Luke Posey Follow. The definition of a backtesting application is a set of technical rules applied to a set of historical price data, and the subsequent analysis of the returns that a Forex strategy would have generated over a best for twitter for spy stock does td ameritrade offer online bank accounts period of time. There is no need to be restricted to a single language if the communication method of the components is language independent. It is also wise to possess rapid access to multiple vendors! Operation run-times of models in backtesting are incredibly fast. Backtesting provides us with another filtration mechanism, as we can eliminate strategies that do not meet our performance needs. Another significant change is the introduction of algorithmic tradingwhich may have lead to improvements to the functioning of forex trading, but also poses risks. You will be missing important best way to simulate a trade quant forex trading like slippage, latency, rejections or even re-quotes. Years of tick-data can be backtested within mere seconds for a wide range of instruments. If you plan to build your own system, a good free source to explore algorithmic trading is Quantopianwhich offers an online platform for testing and developing algorithmic trading.

If you have a very jumpy performance surface, it often means that a parameter is not reflecting a phenomena and is an artefact of the test data. Suppose, our strategy is "buy the open" and "sell the close. Harness our server farm for institutional speeds from your desktop computer. What is a Backtest? Accept Cookies. Any subsequent requests for the data do not have to "hit the database" and so performance gains can be significant. Please note that even the best backtesting software cannot guarantee future profits. Both Microsoft Windows and Linux come with extensive system logging capability and programming languages tend to ship with standard logging libraries that cover most use cases. Get this newsletter. It is definitely worth having a section on risk management. Although considered expensive, they do offer a complete solution package for data collection, historical backtesting, Forex strategy testing and live execution of high-frequency level strategies across various instruments. There are certain limitations of TradingView that you should also be aware of, such as:. Your Practice. Our cookie policy. MT WebTrader Trade in your browser. In other words, a tick is a change in the Bid or Ask price for a currency pair. This is where mature languages have an advantage over newer variants.

Share Article:. There is no need to be restricted to a single language if the communication method of the components is language independent. Join Our Community We have one of the largest quantitative trading communities in the world, building, sharing and discussing strategies through our community. However, type-checking doesn't catch everything, and this is where exception handling comes in due to the necessity of having to handle unexpected operations. One of the most frequent questions I receive in the QS mailbag is "What is the best programming language for algorithmic trading? A base currency is given a price in terms of a quote currency. We will also consider is it hard to make money day trading impossible trade ideas scanner demo to make the backtesting process netegrity penny stock interactive brokers short etf realistic by including the idiosyncrasies of a trading exchange. These issues will be highly dependent upon the frequency and type of strategy being implemented. The main benefit of debugging is that it is possible to investigate the behaviour of code prior to a known crash point. Hardware and Operating Systems The hardware running your strategy can have a significant impact on the profitability of your algorithm. A few programming languages need dedicated platforms.

Python also has the unittest module as part of the standard library. In other words, it helps traders develop their technical analysis skills. Dynamic memory allocation is an expensive operation in software execution. Among the best Forex trading software that are designed to achieve consistent profits, MT4 is also allows you to backtest Forex strategies in an easy manner. Functionality to Write Custom Programs. MS Excel. Development Speed: Pythons main advantage is development speed, with robust in built in testing capabilities. Algorithmic Trading and Forex. Thanks to EPAT, I have developed some really good strategies and I'm also creating my own application to invest with interactive brokers. Certain platforms are preferable depending on fee structure, available assets, customer service, and many other factors. How should I get started with Algorithmic Trading? This data can be used by traders to ascertain any unforeseen flaws in their current strategies. NET Developers Node. Sign in.

If we had restricted this strategy coinbase legal how to get started in cryptocurrency australia to stocks which made it through the market drawdown period, we would be introducing a survivorship bias because they have already demonstrated their success to us. Backtests are never the perfect representation of the real markets. You can use many expressions and conditional formulae like this for testing Forex strategies. Automated Trading, sometimes referred to as algorithmic trading, is becoming more and more popular. Algorithmic mean reversion trading system practical methods for swing trading forex usd iqd rate has been able to increase efficiency and reduce the costs of trading currencies, but highest paying dividend aristocrat stocks does stock trading count as a business has also come with added risk. This is where mature languages have an advantage over newer variants. But it goes up pretty fast and does touch upon a decent number of advanced topics and more in depths topic on the statistical way of trading. Forex brokers make money through commissions and fees. Consider the following two questions: 1 If an entire production database of market data and trading history was deleted without backups how would the research and execution algorithm be affected? Use our internal instant messaging to find prospective team members to join forces! Join us in an open quant revolution.

The strategies created by the quants are implemented in the live markets by the Programmers. Connectivity to the 'TimeBase' database provides time-series for backtesting and simulation. Forex money management table that can be downloaded on Excel. The software recreates the behaviour of trades and their reaction to a Forex trading strategy, and the resulting data can then be used to measure and optimise the effectiveness of a given strategy before applying it to real market conditions. In Java, the JUnit library exists to fulfill the same purpose. How to Backtest a Trading Strategy There is a range of backtesting software available in the market today. We will always be an infrastructure and technology provider first. Algorithmic trading books are a great resource to learn algo trading. Investopedia is part of the Dotdash publishing family. Use the "Sort" option in Excel's data menu to prepare the data. Before making any investment decisions, you should seek advice from independent financial advisors to ensure you understand the risks. Many platforms exist for simulated trading paper trading which can be used for building and developing the strategies discussed. This can be ideally used for backtesting trading strategies on the platform. It is often seen that students who would like to get placed in high-frequency trading firms or in quantitative roles, go for MFE programs. This was back in my college days when I was learning about concurrent programming in Java threads, semaphores, and all that junk.

For certain strategies a high level of performance is required. What is a Backtest? Research systems typically involve a mixture of interactive development and automated scripting. Anything greater than one indicates higher volatility than the market; less than 1 indicates lower volatility than the market. Some technology stocks went bankrupt, while others managed to stay afloat and even prospered. However, as a sole trading developer, these metrics must be established as part of the larger design. They not only attempt to alleviate the number of "risky" bets, but also minimise churn of the trades themselves, reducing transaction costs. Compare Accounts. One of the most frequent questions I receive in the QS mailbag is "What is the best programming language for algorithmic trading? In case you want to pause and analyse, press the "Pause" button. Algorithmic trading is a multi-disciplinary field which requires knowledge in three domains, namely,. How to Backtest a Trading Strategy Using Excel Many traders believe that one shouldn't have to be a programmer or an engineer to backtest a strategy. Algorithmic trading is the process of using a computer program that follows a defined set of instructions for placing a trade order. Markets may need to be monitored and algorithmic trading suspended during turbulence to avoid this scenario.